All Categories

Featured

Table of Contents

Annuities are insurance policy products that can eliminate the threat you'll outlive your retired life savings. Today, because fewer individuals are covered by typical pension plans, annuities have actually become progressively prominent. They can typically be integrated with other insurance coverage items, like life insurance policy, to produce total protection for you and your family. It's usual today for those approaching retired life to be worried about their cost savings and for how long they will certainly last.

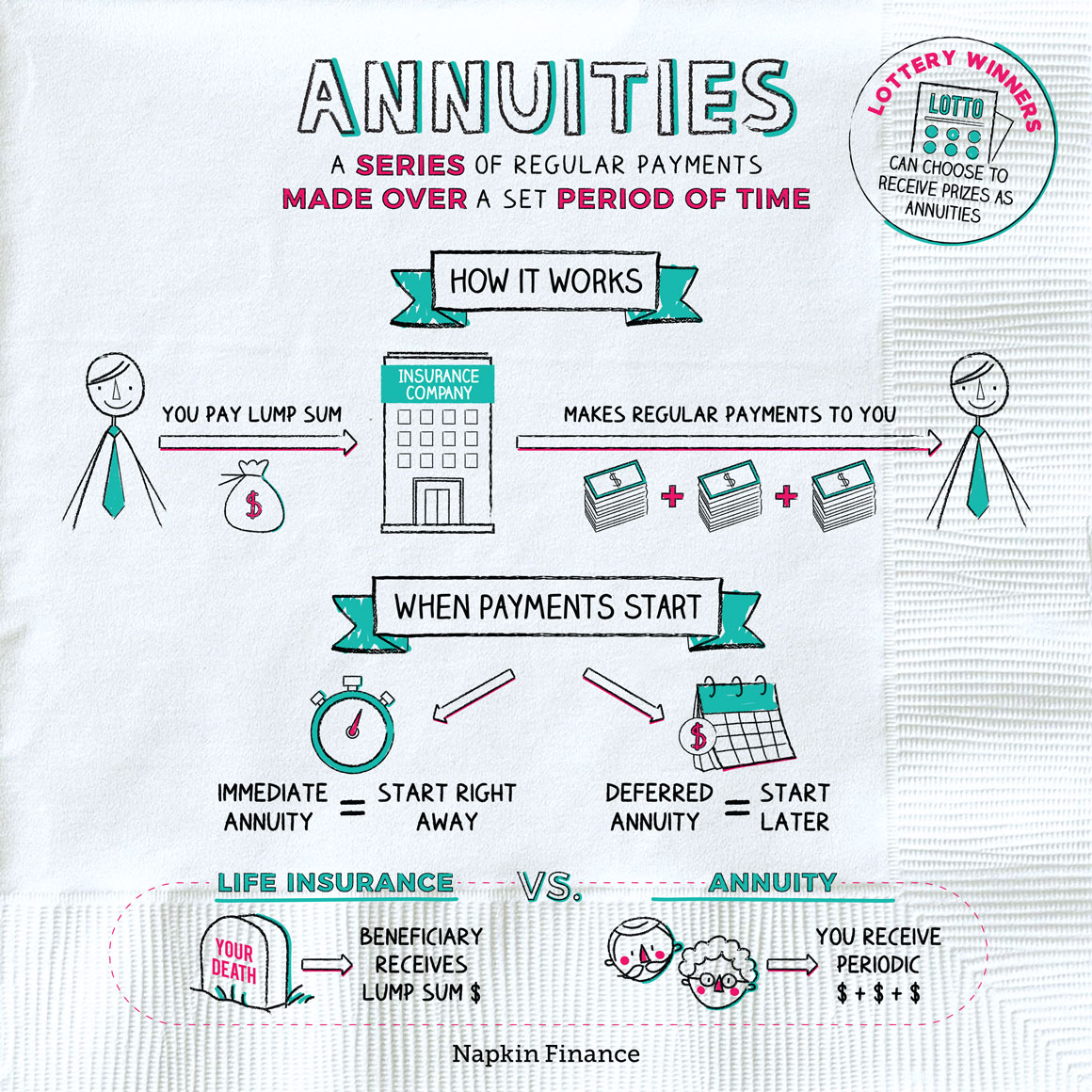

You make an exceptional repayment to an insurance policy business, either in a swelling sum or as a series of repayments. In return, you'll obtain routine revenue for a given period, typically for life.

Annuities are no different. Take a look at some of the key advantages of annuities contrasted with various other retired life savings lorries: Annuities are the only monetary item that can offer you with guaranteed lifetime revenue and guarantee that you are never at risk of outlasting your financial savings.

As holds true with many retirement savings automobiles, any incomes on your deferred annuity are tax-deferred. That indicates you don't pay tax obligations on the development in your account up until you withdraw it or begin taking payouts. In other words, the taxes you 'd typically owe on the gains every year continue to be in your account and grow, commonly leaving you with higher equilibriums later on.

What does an Annuity Interest Rates include?

1 To locate the ideal item for you, you'll need to shop around among trusted insurance policy companies. Among the benefits of annuities is that they are extremely personalized. The right annuity for you is going to depend upon numerous elements, including your age, your present savings, exactly how long you require the income, and any type of defenses you may want.

2 Below are a pair of usual instances: You and your spouse are planning to retire within the next couple of years. You've both saved an excellent amount yet are now attempting to problem the numbers and see to it your savings will last. It's usual to worry over just how much of your cost savings to gain access to each year, or just how long your savings will need to last.

3 That way, you and your partner will have earnings you can rely on no matter what happens. On the other hand, let's say that you're in your late 20s. You've recently had a good raise at the workplace, and you desire to see to it you're doing every little thing you can to assure a comfortable retirement.

Retirement is a long way off, and that understands just how much those financial savings will grow or if there will certainly be sufficient when you get to retirement age. Some annuities allow you to make superior settlements every year.

Tax-deferred Annuities

The annuity will have the chance to experience growth, yet it will additionally be subject to market volatility. New York Life has many options for annuities, and we can help you tailor them to your household's one-of-a-kind requirements.

The buyer is often the annuitant and the person to whom periodic payments are made. There are 2 fundamental type of annuity agreements: immediate and delayed. An instant annuity is an annuity agreement in which payments begin within twelve month of the date of purchase. The instant annuity is acquired with a single costs and regular repayments are usually equal and made regular monthly, quarterly, semi-annually or each year.

Periodic repayments are delayed until a maturation date mentioned in the agreement or, if earlier, a date chosen by the owner of the contract - Fixed vs variable annuities. The most usual Immediate Annuity Contract payment options include: Insurer makes periodic repayments for the annuitant's life time. A choice based upon the annuitant's survival is called a life set choice

There are 2 annuitants (called joint annuitants), typically spouses and routine payments proceed until the fatality of both. The income payment amount may continue at 100% when just one annuitant lives or be minimized (50%, 66.67%, 75%) during the life of the enduring annuitant. Regular payments are created a given period of time (e.g., 5, 10 or two decades).

Why is an Deferred Annuities important for my financial security?

Some immediate annuities provide rising cost of living security with regular boosts based upon a set price (3%) or an index such as the Consumer Cost Index (CPI). An annuity with a CPI modification will begin with reduced settlements or need a higher initial costs, yet it will certainly supply at least partial protection from the danger of rising cost of living. Secure annuities.

Income settlements stay constant if the financial investment efficiency (after all costs) equates to the assumed investment return (AIR) stated in the agreement. Immediate annuities typically do not permit partial withdrawals or give for cash abandonment benefits.

Such individuals should look for insurance providers that make use of low-grade underwriting and think about the annuitant's wellness status in establishing annuity revenue payments. Do you have enough funds to fulfill your earnings needs without purchasing an annuity? Simply put, can you handle and take organized withdrawals from such sources, without concern of outliving your sources? If you are concerned with the risk of outlasting your funds, after that you could take into consideration purchasing a prompt annuity at least in a quantity sufficient to cover your fundamental living costs.

What are the benefits of having an Guaranteed Return Annuities?

For some options, your wellness and marital standing might be taken into consideration. A straight life annuity will offer a higher monthly revenue payment for a provided costs than life contingent annuity with a duration particular or reimbursement attribute. Simply put, the price of a specific income payment (e.g., $100 monthly) will certainly be greater for a life contingent annuity with a period specific or reimbursement feature than for a straight life annuity.

For instance, a person with a dependent partner might intend to think about a joint and survivor annuity. A person worried about obtaining a minimum return on his/her annuity premium may want to think about a life set alternative with a period specific or a refund attribute. A variable immediate annuity is usually selected to equal inflation during your retired life years.

A paid-up deferred annuity, likewise generally described as a deferred income annuity (DIA), is an annuity agreement in which each costs repayment acquisitions a fixed buck income advantage that commences on a defined day, such as an individual's retirement day. The agreements do not maintain an account worth. The premium expense for this product is a lot less than for a prompt annuity and it allows a person to preserve control over the majority of his/her various other properties during retirement, while securing longevity defense.

{kind=link}

Table of Contents

Latest Posts

Exploring Fixed Index Annuity Vs Variable Annuities Key Insights on Variable Annuity Vs Fixed Indexed Annuity Defining Variable Annuity Vs Fixed Annuity Features of Smart Investment Choices Why Choosi

Decoding Variable Annuities Vs Fixed Annuities Key Insights on Your Financial Future What Is Fixed Vs Variable Annuities? Pros and Cons of Retirement Income Fixed Vs Variable Annuity Why Choosing the

Analyzing Fixed Interest Annuity Vs Variable Investment Annuity A Closer Look at How Retirement Planning Works What Is Fixed Interest Annuity Vs Variable Investment Annuity? Benefits of Choosing the R

More

Latest Posts